{kind=link}

The depreciation of the Ghanaian Cedi has now become a perennial crisis. Overtime, we have come to the realization that the depreciation of the currency is structural and not necessarily due any form of mismanagement of the economy by the government in power. This mainly because this trend of annual depreciation is historical and successive governments have failed to stall its occurrence.

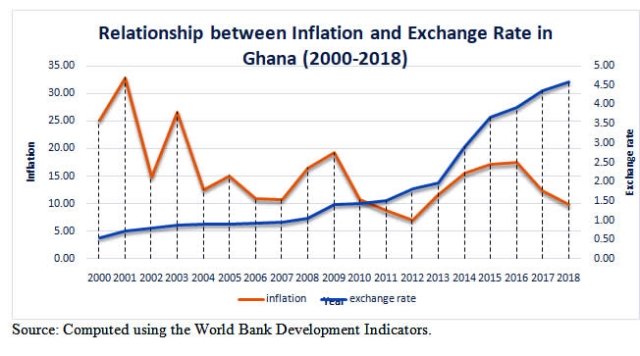

Ghana’s current vice president, Dr. Bawumia, in a series of public lectures, highlighted the discrepancy between the exchange rate and inflation. Figure 1 below provides anecdotal evidence of the continuous discrepancy between inflation and exchange rate overtime in Ghana.

Discrepancy between inflation and exchange rate

The theoretical underpinning of the relationship between inflation and exchange rates is the relative purchasing power parity (PPP). Through PPP, the appreciation or depreciation of the exchange rate should be equalled to inflation rate differentials. However, empirical evidence has shown that this is far from the reality. For instance, the Big Mac Index built by the Economist newspaper tests this theory using price of McDonald’s Big Mac burger. The burger is used because it is a well-known and globally uniformed consumer product. The index shows that the PPP theory is not empirically feasible, especially in the short-run as the index shows a discrepancy between the market and PPP implied exchange rates.

The discrepancy between the exchange rate and inflation is due to the irrationality of certain assumptions under which the PPP theory was formulated. First, the assumption of zero transaction cost in the goods markets is not realistic. This assumption means that trade is frictionless and that there are no transportation and tariff costs when goods cross borders. Second, the assumption that all goods are tradable. Most tangible goods have both the tradable and non-tradable components. The intractability of these assumptions makes it difficult to assume that a simple relationship between inflation and exchange rate exists. This is relevant today in Ghana as we still witnessing a drifting apart of inflation and exchange rates, especially from 2016. However, a myriad of empirical evidence has shown that the PPP theory holds in the long-run as price level and exchange rate drift together along a common trend.

Fundamental causes of depreciation

The depreciation or appreciation of the Ghana Cedi is fundamentally determined by the supply and demand for US dollars (USD) in Ghana. The supply of USD is mainly from foreign reserves which is dependent on the amount of foreign exchange we receive from exports and foreign aid. With Ghana now classified as a lower middle-income country, the foreign aid component would continuously dwindle. Demand for USD also comes mainly from our insatiable demand for foreign goods in Ghana. Increased foreign consumption leads to an increase in demand for USD, thereby mounting incessant pressure on the Cedi.

Another major cause of the depreciation is the dollarization of the Ghanaian economy, where goods and services are being priced illegally in USD. This is mostly done by foreign companies operating in Ghana (international airlines, hotels, etc.) When you are buying KLM ticket in Denmark, the prices of the tickets are quoted in Danish Kroner, not Euro or USD. Even the government of Ghana is culpable when it comes to pricing in USD. For instance, the container import charges such as port dues and stevedoring charges are all priced in USD at our ports. Even in situations where goods and services are quoted in local currency, the Cedi equivalents are quoted using higher exchange rates. As a result, customers will prefer to pay in USD instead of the Cedi equivalents that are pegged at arbitrarily determined exchange rates.

The depreciation of the Cedi can be a blessing in disguise as it could make our exports cheaper and Ghanaian exports more competitive internationally. However, there is a condition (the Marshall Lerner Condition) which stipulates that devaluation will improve the devaluing nation’s trade balance if the sum of the devaluing nation’s demand elasticity for imports plus the foreign nation’s demand elasticity for exports is greater than one. This potential benefit associated with depreciation is undermined because the Ghanaian economy is import-dependent.

The way forward

A short-term solution to stall the free fall of the Ghanaian Cedi is a clamp down on the dollarization of the economy. Foreign or local companies must not be allowed to price their goods and services in USD in Ghana. In addition, individuals without foreign sources of income should not be allowed to save in foreign currencies. The subtle practice of pricing in local currency but pegged to some arbitrarily exchange rate should be discouraged. If the government is able to discourage such negative practices, the demand for USD in Ghana will decrease and thus bring some stability to the economy.

Concerns about the exchange rate is not only limited to the devaluation, but also the persistent volatility or continuous fluctuation in the exchange rate. I am certain most importers would prefer an exchange rate of say GHC20=USD 1 to GH6=USD 1, if the higher rate will have a lower volatility. For the purpose of planning, importers or business owners would prefer a higher exchange rate with lower volatility to a lower exchange rate with higher volatility. Higher volatility creates uncertainty about international transactions.

The management of the economy should not be limited to the current government. Government must embrace a holistic approach by bringing all stakeholders to the drawing board to think through and devise short and long-term solutions to tackle this economic canker. This is important because the time for long-term solutions will surpass the political term of any government. In addition, we should intensify the political independence of the central bank and stop politicizing some of these state institutions, only then can we hold the technocrats responsible and not politicians. It is the sole responsibility of the Bank of Ghana to ensure the stability of our local currency.

Source: Dr. S. Kwaku Afesorgbor | Centre for Trade Analysis and Development